UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

SCHEDULE TO/A

Tender Offer Statement Pursuant to Section 14(d)(1) or 13(e)(1)

of the Securities Exchange Act of 1934

(Amendment No. 1)

Warner Bros. Discovery, Inc.

(Name of Subject Company (Issuer))

Prince Sub Inc.

(Offeror)

a direct wholly owned subsidiary of

Paramount Skydance Corporation

(Parent of Offeror)

(Names of Filing Persons (identifying status as offeror, issuer or other person))

Series A Common Stock, par value $0.01 per share

(Title of Class of Securities)

934423104

(CUSIP Number of Class of Securities)

Makan Delrahim

Chief Legal Officer

Paramount Skydance Corporation

1515 Broadway

New York, New York 10036

(212) 258-6000

(Name, Address and Telephone Number of Person Authorized to Receive Notices and Communications on Behalf of Filing Persons)

With a copy to:

Copies to:

| Faiza J. Saeed Andrew J. Pitts C. Daniel Haaren Daniel J. Cerqueira Claudia J. Ricciardi Alexander E. Greenberg Cravath, Swaine & Moore LLP Two Manhattan West 375 Ninth Avenue New York, New York 10001 (212) 474-1000 |

Ian Nussbaum Max Schleusener Latham & Watkins LLP 1271 Avenue of the Americas New York, New York 10020 (212) 906-1200 |

| ☐ | Check the box if the filing relates solely to preliminary communications made before the commencement of a tender offer. |

Check the appropriate boxes below to designate any transactions to which the statement relates:

| ☒ | third-party tender offer subject to Rule 14d-1. |

| ☐ | issuer tender offer subject to Rule 13e-4. |

| ☐ | going-private transaction subject to Rule 13e-3. |

| ☐ | amendment to Schedule 13D under Rule 13d-2. |

Check the following box if the filing is a final amendment reporting the results of the tender offer: ☐

If applicable, check the appropriate box(es) below to designate the appropriate rule provision(s) relied upon:

| ☐ | Rule 13e-4(i) (Cross-Border Issuer Tender Offer) |

| ☐ | Rule 14d-1(d) (Cross-Border Third-Party Tender Offer) |

This Amendment No. 1 to Schedule TO (together with any exhibits and annexes attached hereto, and as it may be amended or supplemented from time to time, this “Amendment”) is filed by (i) Prince Sub Inc., a Delaware corporation (the “Purchaser”) and a direct wholly owned subsidiary of Paramount Skydance Corporation, a Delaware corporation (“Paramount”), and (ii) Paramount and amends and supplements the Tender Offer Statement on Schedule TO filed with the U.S. Securities and Exchange Commission (the “SEC”) on December 8, 2025 (together with any amendments and supplements thereto, the “Schedule TO”) by the Purchaser and Paramount. This Schedule TO relates to the offer by the Purchaser to purchase all of the outstanding shares of Series A Common Stock, par value $0.01 per share (the “Shares”), of Warner Bros. Discovery, Inc., a Delaware corporation (“Warner Bros.”), at $30.00 per share, net to the seller in cash, without interest and less any required withholding taxes, upon the terms and subject to the conditions set forth in the Offer to Purchase, dated December 8, 2025 (as it may be amended or supplemented from time to time, the “Offer to Purchase”), a copy of which is attached as Exhibit (a)(1)(A) to the Schedule TO filed with the SEC on December 8, 2025, and in the related Letter of Transmittal (as it may be amended or supplemented from time to time, the “Letter of Transmittal,” and together with the Offer to Purchase, the “Offer”), a copy of which is attached as Exhibit (a)(1)(B) to the Schedule TO filed with the SEC on December 8, 2025.

Except as otherwise set forth in this Amendment, the information in Schedule TO remains unchanged and is incorporated herein by reference to the extent relevant to the items in this Amendment. Capitalized terms used but not defined herein have the meanings ascribed to them in the Schedule TO.

Item 12. Exhibits

Item 12 of the Schedule TO is also hereby amended and supplemented by adding the following exhibits.

| (a)(5)(B) |

Investor Presentation of Paramount, dated December 8, 2025 | |

| (a)(5)(C) |

Transcript of Interview by David Ellison, Chairman and CEO of Paramount, dated as of December 8, 2025 | |

| (a)(5)(D) |

Transcript of Analyst and Media Call by Paramount executives, dated as of December 8, 2025 | |

SIGNATURE

After due inquiry and to the best of my knowledge and belief, I certify that the information set forth in this statement is true, complete and correct.

Dated: December 8, 2025

| PARAMOUNT SKYDANCE CORPORATION | ||

| By: | /s/ Stephanie Kyoko McKinnon | |

| Name: Stephanie Kyoko McKinnon | ||

| Title: General Counsel | ||

| PRINCE SUB INC. | ||

| By: | /s/ Stephanie Kyoko McKinnon | |

| Name: Stephanie Kyoko McKinnon | ||

| Title: General Counsel | ||

EXHIBIT INDEX

Exhibit (a)(5)(B) Paramount’s $30 all-cash offer provides greater value and certainty to WBD shareholders December 8, 2025

Disclaimer This presentation is provided for informational purposes only and for no other purpose. Certain information contained herein has been obtained from published sources prepared by third parties that Paramount Skydance Corporation (“Paramount”) believes to be reliable. Moreover, certain information in this presentation is based on assumptions, estimates and other factors that were available to Paramount at the time this presentation was prepared. Such assumptions, estimates or other factors, whether made by Paramount or third parties, may prove to be, or become, incorrect, thus rendering the information in this presentation inaccurate, incomplete or incorrect. Paramount has not made any independent review of information based on public statistics or information from third parties regarding the market information that has been provided by such third parties. Paramount has no obligation to update such information, including in the event that such information becomes inaccurate. Paramount may own or have rights to various trademarks, service marks and trade names that it uses in connection with the operation of its business. This presentation may also contain trademarks, service marks, trade names and copyrights of third parties, which are the property of their respective owners. The use or display of third parties’ trademarks, service marks, trade names or products in this presentation is not intended to, and does not imply, a relationship with Paramount, or an endorsement or sponsorship by or of Paramount. Solely for convenience, the trademarks, services marks, trade names and copyrights referred to in this presentation may appear without the TM, SM, © or ® symbols, but such references are not intended to indicate, in any way, that Paramount will not assert, to the fullest extent under applicable law, its rights or the right of the applicable licensor, to these trademarks, service marks, trade names and copyrights. Cautionary Note Regarding Forward-Looking Statements This presentation contains both historical and forward-looking statements, including statements related to Paramount’s future financial results and performance, potential achievements, anticipated reporting segments and industry changes and developments. All statements that are not statements of historical fact are, or may be deemed to be, “forward-looking statements”. Similarly, statements that describe Paramount’s objectives, plans or goals are or may be forward-looking statements. These forward-looking statements reflect Paramount’s current expectations concerning future results and events; generally can be identified by the use of statements that include phrases such as “believe,” “expect,” “anticipate,” “intend,” “plan,” “foresee,” “likely,” “will,” “may,” “could,” “estimate” or other similar words or phrases; and involve known and unknown risks, uncertainties and other factors that are difficult to predict and which may cause Paramount’s actual results, performance or achievements to be different from any future results, performance or achievements expressed or implied by these statements. These risks, uncertainties and other factors include, among others: the outcome of the tender offer by the Company and Prince Sub Inc. (the “Tender Offer”) to purchase for cash all of the outstanding Series A common stock of Warner Bros. Discovery, Inc. (“Warner Bros. Discovery”) or any discussions between Paramount and Warner Bros. Discovery with respect to a possible transaction (including, without limitation, by means of the Tender Offer, the “Potential Transaction”), including the possibility that the Tender Offer will not be successful, that the parties will not agree to pursue a business combination transaction or that the terms of any such transaction will be materially different from those described herein, the conditions to the completion of the Potential Transaction or the previously announced transaction between Warner Bros. and Netflix Inc. (“Netflix”) pursuant to the Agreement and Plan of Merger, dated December 4, 2025, among Netflix, Nightingale Sub, Inc., Warner Bros. and New Topco 25, Inc. (the “Proposed Netflix Transaction”), including the receipt of any required stockholder and regulatory approvals for either transaction, the proposed financing for the Potential Transaction, the indebtedness Paramount expects to incur in connection with the Potential Transaction and the total indebtedness of the combined companies, the possibility that Paramount may be unable to achieve expected synergies and operating efficiencies within the expected timeframes or at all and to successfully integrate the operations of Warner Bros. Discovery with those of Paramount, and the possibility that such integration may be more difficult, time-consuming or costly than expected or that operating costs and business disruption (including, without limitation, disruptions in relationships with employees, customers or suppliers) may be greater than expected in connection with the Potential Transaction; risks related to Paramount’s streaming business; the adverse impact on Paramount’s advertising revenues as a result of changes in consumer behavior, advertising market conditions and deficiencies in audience measurement; risks related to operating in highly competitive and dynamic industries, including cost increases; the unpredictable nature of consumer behavior, as well as evolving technologies and distribution models; risks related to Paramount’s decisions to make investments in new businesses, products, services and technologies, and the evolution of Paramount’s business strategy; the potential for loss of carriage or other reduction in or the impact of negotiations for the distribution of Paramount’s content; damage to Paramount’s reputation or brands; losses due to asset impairment charges for goodwill, intangible assets, FCC licenses and content; liabilities related to discontinued operations and former businesses; increasing scrutiny of, and evolving expectations for, sustainability initiatives; evolving business continuity, cybersecurity, privacy and data protection and similar risks; content infringement; domestic and global political, economic and regulatory factors affecting Paramount’s businesses generally, including tariffs and other changes in trade policies; the inability to hire or retain key employees or secure creative talent; disruptions to Paramount’s operations as a result of labor disputes; the risks and costs associated with the integration of, and Paramount’s ability to integrate, the businesses of Paramount Global and Skydance Media, LLC successfully and to achieve anticipated synergies; volatility in the prices of Paramount’s Class B Common Stock; potential conflicts of interest arising from Paramount’s ownership structure with a controlling stockholder; and other factors described in Paramount’s news releases and filings with the Securities and Exchange Commission (the “SEC”), including but not limited to Paramount’s most recent Annual Report on Form 10-K and Paramount’s reports on Form 10-Q and Form 8-K. There may be additional risks, uncertainties and factors that Paramount does not currently view as material or that are not necessarily known. The forward-looking statements included in this presentation are made only as of the date of this report, and Paramount does not undertake any obligation to publicly update any forward-looking statements to reflect subsequent events or circumstances. 2

Disclaimer (cont’d) Additional Information This presentation does not constitute an offer to buy or a solicitation of an offer to sell securities. This communication relates to a proposal that Paramount has made for an acquisition of Warner Bros. Discovery and the Tender Offer that Paramount, through Prince Sub Inc., its wholly owned subsidiary, has made to Warner Bros. Discovery stockholders. The Tender Offer is being made pursuant to a tender offer statement on Schedule TO (including the offer to purchase, the letter of transmittal and other related offer documents), filed with the SEC on December 8, 2025. These materials, as may be amended from time to time, contain important information, including the terms and conditions of the offer. Subject to future developments, Paramount (and, if a negotiated transaction is agreed, Warner Bros. Discovery) may file additional documents with the SEC. This communication is not a substitute for any proxy statement, tender offer statement, or other document Paramount and/or Warner Bros. Discovery may file with the SEC in connection with the proposed transaction. Investors and security holders of Warner Bros. Discovery are urged to read the tender offer statement(s) (including the offer to purchase, the letter of transmittal and other related offer documents), and any other documents filed with the SEC carefully in their entirety if and when they become available as they will contain important information about the proposed transaction. Any definitive proxy statement(s) (if and when available) will be mailed to stockholders of Warner Bros. Discovery. Investors and security holders will be able to obtain free copies of these documents (if and when available) and other documents filed with the SEC by Paramount through the website maintained by the SEC at http://www.sec.gov. This communication is neither a solicitation of a proxy nor a substitute for any proxy statement or other filings that may be made with the SEC. Nonetheless, Paramount and its directors and executive officers and other members of management and employees may be deemed to be participants in the solicitation of proxies against the Proposed Netflix Transaction. You can find information about Paramount’s executive officers and directors in Paramount’s Current Reports on Form 8-K filed with the SEC on August 7, 2025, and September 16, 2025, and Paramount’s Quarterly Report on Form 10-Q filed with the SEC on November 10, 2025. Additional information regarding the interests of such potential participants will be included in one or more proxy statements or other documents filed with the SEC if and when they become available. These documents (if and when available) may be obtained free of charge from the SEC’s website at http://www.sec.gov. 3

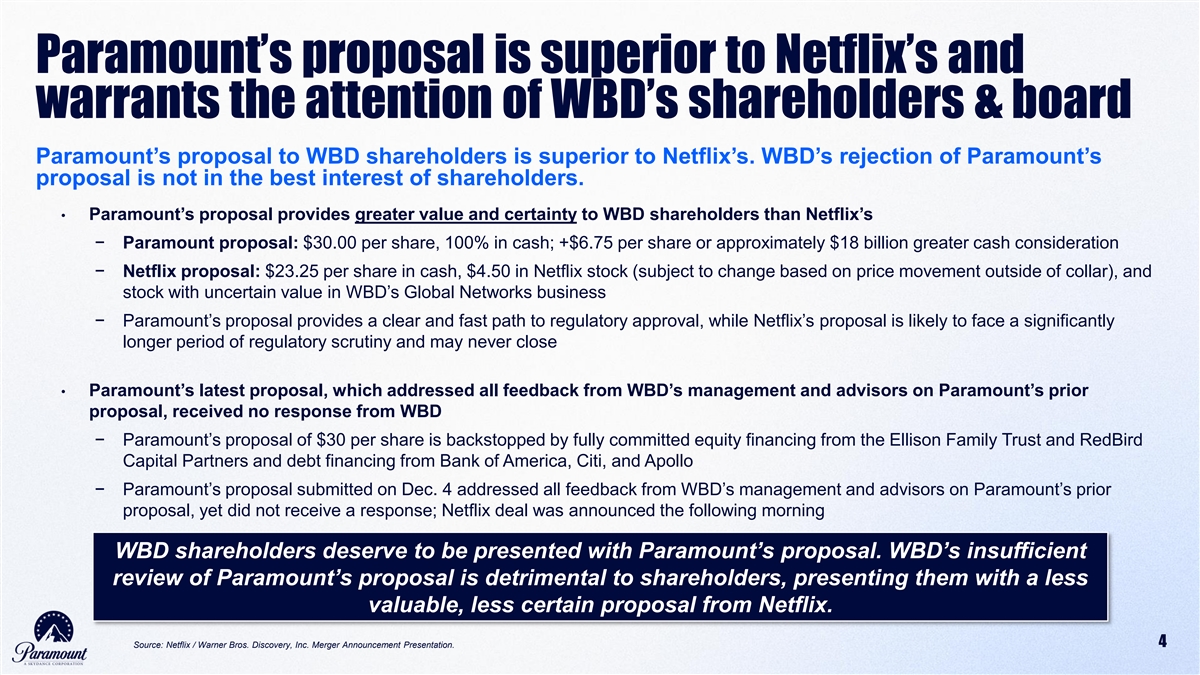

Paramount’s proposal is superior to Netflix’s and warrants the attention of WBD’s shareholders & board Paramount’s proposal to WBD shareholders is superior to Netflix’s. WBD’s rejection of Paramount’s proposal is not in the best interest of shareholders. • Paramount’s proposal provides greater value and certainty to WBD shareholders than Netflix’s 1 − Paramount proposal: $30.00 per share, 100% in cash; +$6.75 per share or approximately $18 billion greater cash consideration − Netflix proposal: $23.25 per share in cash, $4.50 in Netflix stock (subject to change based on price movement outside of collar), and stock with uncertain value in WBD’s Global Networks business 2 − Paramount’s proposal provides a clear and fast path to regulatory approval, while Netflix’s proposal is likely to face a significantly longer period of regulatory scrutiny and may never close • Paramount’s latest proposal, which addressed all feedback from WBD’s management and advisors on Paramount’s prior proposal, received no response from WBD 3 − Paramount’s proposal of $30 per share is backstopped by fully committed equity financing from the Ellison Family Trust and RedBird Capital Partners and debt financing from Bank of America, Citi, and Apollo − Paramount’s proposal submitted on Dec. 4 addressed all feedback from WBD’s management and advisors on Paramount’s prior proposal, yet did not receive a response; Netflix deal was announced the following morning WBD shareholders deserve to be presented with Paramount’s proposal. WBD’s insufficient review of Paramount’s proposal is detrimental to shareholders, presenting them with a less valuable, less certain proposal from Netflix. Source: Netflix / Warner Bros. Discovery, Inc. Merger Announcement Presentation. 4

Paramount’s proposal is superior to Netflix’s proposal across all aspects Paramount’s Proposal Provides WBD Shareholders with More Value and More Certainty Key Consideration Paramount Netflix Only Streaming & Studios Business 100% of Warner Bros. Discovery Scope✓✗ (Excludes Global Networks Business) $30.00 per share $23.25 per share Cash Consideration ✓✗ (+$6.75 per share / +$18bn incremental / +29% more value) $30.00 per share $27.75 per share Total Consideration ✓✗ (+$2.25 per share / +8% more value) (includes $4.50 per share in Netflix Stock) $30.00 per share ~$28.75 per share Total Offer Value ✓✗ (+$1.25 per share / +4% more value) (includes ~$1.00 per share in Global Networks Stock) Less certainty of value given significant uncertainty of Linear Networks ‘stub’ All cash proposal for entire company equity value, leaving shareholders exposed to a highly-levered and structurally Value Certainty✗ ✓ provides clear value certainty declining asset Paramount has a clear path to regulatory approval and it provides for Much more challenging approvals and later “Outside Date” underscores Closing Certainty ✓✗ superior closing certainty and protections for WBD’s shareholders proposal’s regulatory uncertainty Paramount’s proposal expects to receive regulatory approvals Netflix proposal is likely to face a significantly longer regulatory approval Timing ✓✗ (likely within 12 months) process (or be blocked entirely), delaying value realization Committed to exhaustive regulatory efforts, up to a material adverse effect Netflix agreed to more limited regulatory efforts, with no obligations to do on the entire Combined Company, with regulatory process started in Regulatory Commitment ✗ ✓ anything to its existing business multiple regions Total consideration and value of NFLX stock component of consideration are subject to change. Should less debt than expected be placed on Global Networks, NFLX’s $27.75 will be reduced on a dollar-for-dollar basis. th Should NFLX stock trade below the collar range, WBD shareholders may receive less value than $4.50 per share. As of Dec. 5 , NFLX stock was only trading ~2% above the low-end of 5 the agreed collar range, following a ~3% drop the day of announcement and ~20% drop since NFLX Q3 earnings and initial rumors of WBD pursuit Source: Netflix / Warrner Bros. Discovery, Inc. Merger Announcement Presentation.

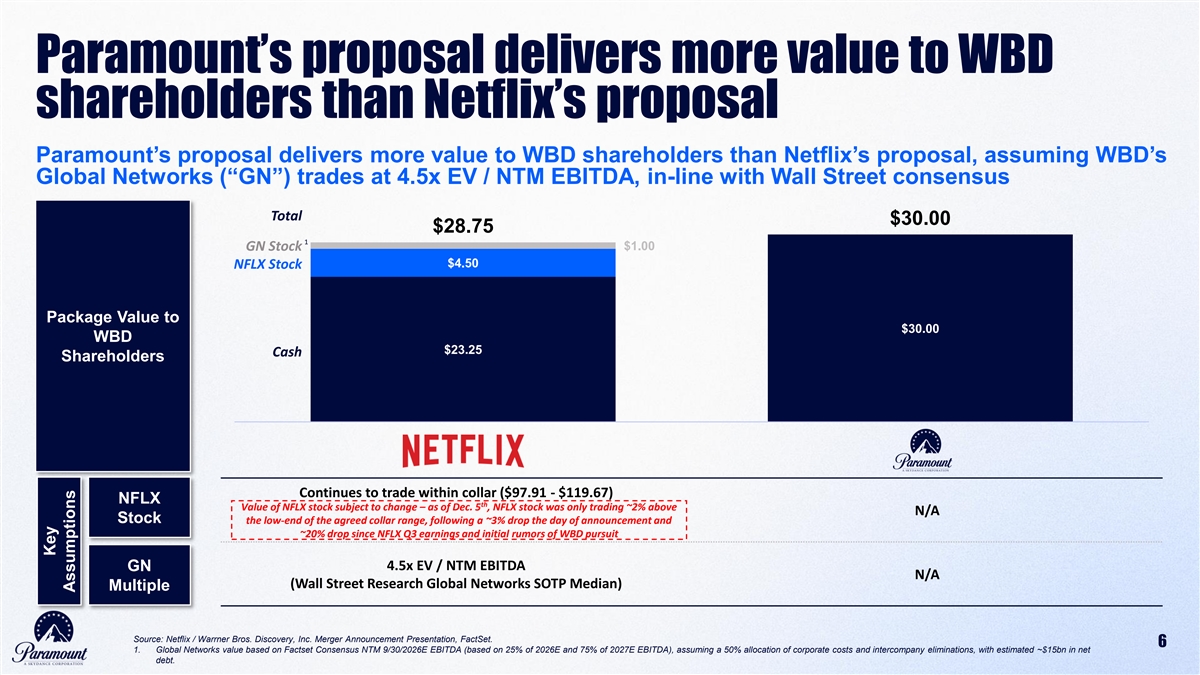

Paramount’s proposal delivers more value to WBD shareholders than Netflix’s proposal Paramount’s proposal delivers more value to WBD shareholders than Netflix’s proposal, assuming WBD’s Global Networks (“GN”) trades at 4.5x EV / NTM EBITDA, in-line with Wall Street consensus Total $30.00 $28.75 1 $1.00 GN Stock $4.50 NFLX Stock Package Value to $30.00 WBD $23.25 Cash Cash Shareholders Continues to trade within collar ($97.91 - $119.67) NFLX th Value of NFLX stock subject to change – as of Dec. 5 , NFLX stock was only trading ~2% above N/A Stock the low-end of the agreed collar range, following a ~3% drop the day of announcement and ~20% drop since NFLX Q3 earnings and initial rumors of WBD pursuit 4.5x EV / NTM EBITDA GN N/A (Wall Street Research Global Networks SOTP Median) Multiple Source: Netflix / Warrner Bros. Discovery, Inc. Merger Announcement Presentation, FactSet. 6 1. Global Networks value based on Factset Consensus NTM 9/30/2026E EBITDA (based on 25% of 2026E and 75% of 2027E EBITDA), assuming a 50% allocation of corporate costs and intercompany eliminations, with estimated ~$15bn in net debt. Key Assumptions

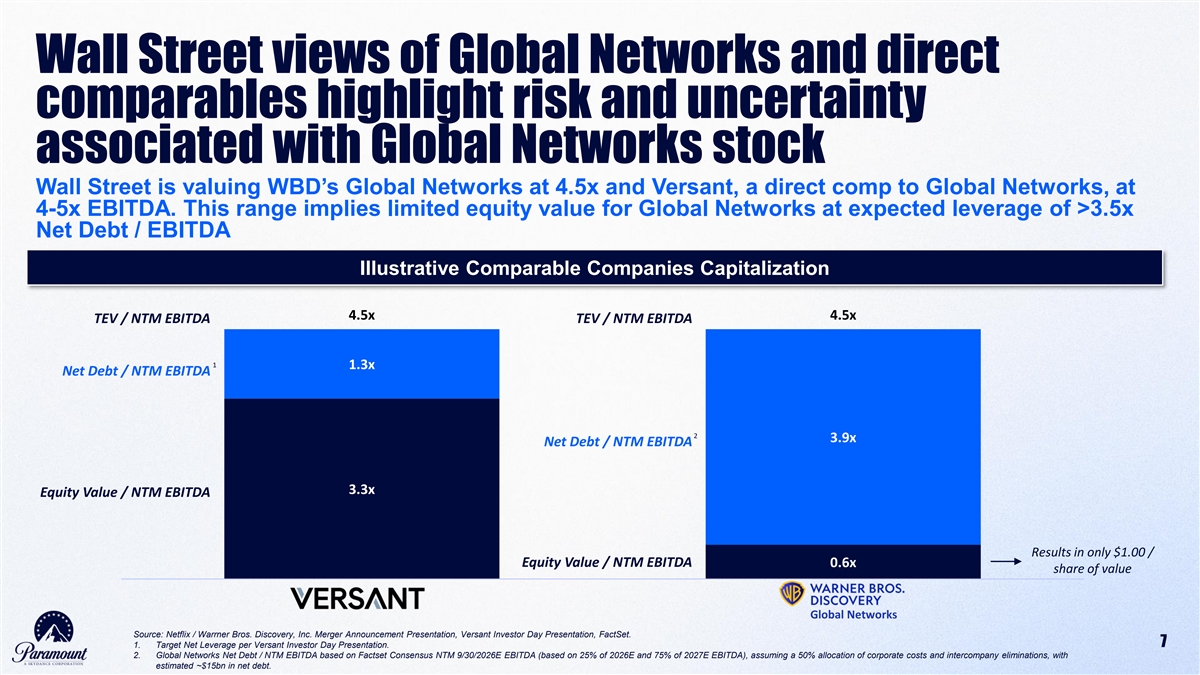

Wall Street views of Global Networks and direct comparables highlight risk and uncertainty associated with Global Networks stock Wall Street is valuing WBD’s Global Networks at 4.5x and Versant, a direct comp to Global Networks, at 4-5x EBITDA. This range implies limited equity value for Global Networks at expected leverage of >3.5x Net Debt / EBITDA Illustrative Comparable Companies Capitalization 4.5x 4.5x TEV / NTM EBITDA TEV / NTM EBITDA 1 1.3x Net Debt / NTM EBITDA 2 3.9x Net Debt / NTM EBITDA 3.3x Equity Value / NTM EBITDA Results in only $1.00 / Equity Value / NTM EBITDA 0.6x share of value Global Networks Source: Netflix / Warrner Bros. Discovery, Inc. Merger Announcement Presentation, Versant Investor Day Presentation, FactSet. 1. Target Net Leverage per Versant Investor Day Presentation. 7 2. Global Networks Net Debt / NTM EBITDA based on Factset Consensus NTM 9/30/2026E EBITDA (based on 25% of 2026E and 75% of 2027E EBITDA), assuming a 50% allocation of corporate costs and intercompany eliminations, with estimated ~$15bn in net debt.

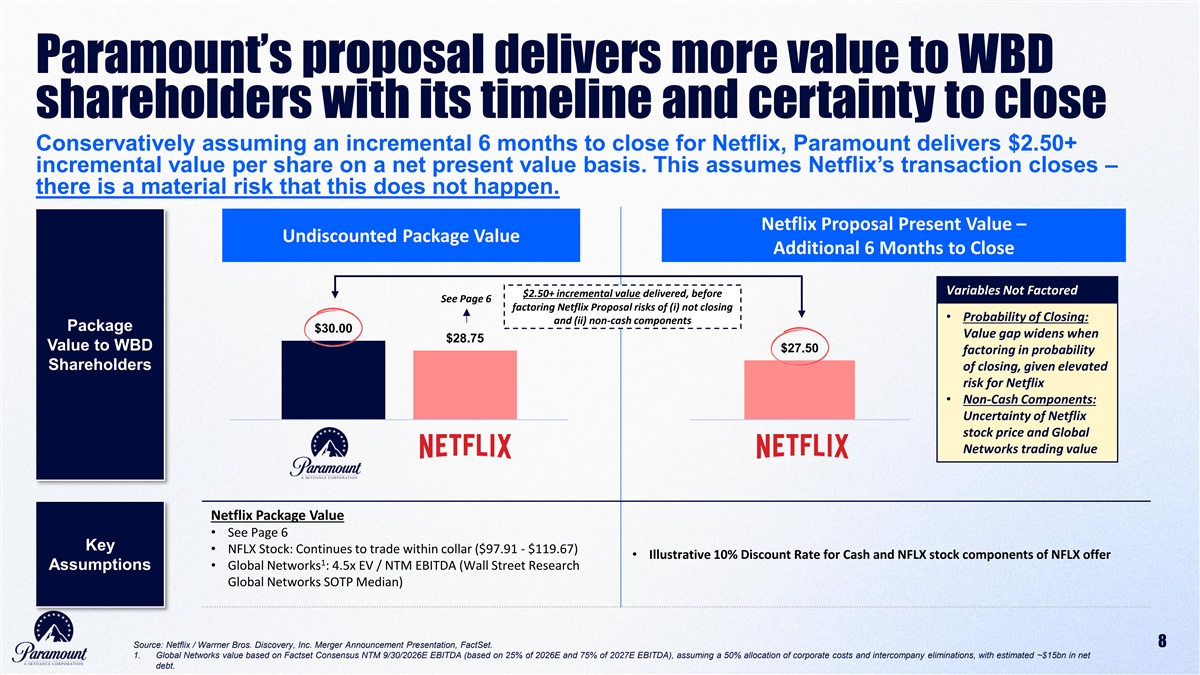

Paramount’s proposal delivers more value to WBD shareholders with its timeline and certainty to close Conservatively assuming an incremental 6 months to close for Netflix, Paramount delivers $2.50+ incremental value per share on a net present value basis. This assumes Netflix’s transaction closes – there is a material risk that this does not happen. Netflix Proposal Present Value – Undiscounted Package Value Additional 6 Months to Close Variables Not Factored $2.50+ incremental value delivered, before See Page 6 factoring Netflix Proposal risks of (i) not closing • Probability of Closing: and (ii) non-cash components Package $30.00 Value gap widens when $28.75 Value to WBD $27.50 factoring in probability Shareholders of closing, given elevated risk for Netflix • Non-Cash Components: Uncertainty of Netflix stock price and Global Networks trading value Netflix Package Value • See Page 6 Key • NFLX Stock: Continues to trade within collar ($97.91 - $119.67) • Illustrative 10% Discount Rate for Cash and NFLX stock components of NFLX offer 1 Assumptions • Global Networks : 4.5x EV / NTM EBITDA (Wall Street Research Global Networks SOTP Median) Source: Netflix / Warrner Bros. Discovery, Inc. Merger Announcement Presentation, FactSet. 8 1. Global Networks value based on Factset Consensus NTM 9/30/2026E EBITDA (based on 25% of 2026E and 75% of 2027E EBITDA), assuming a 50% allocation of corporate costs and intercompany eliminations, with estimated ~$15bn in net debt.

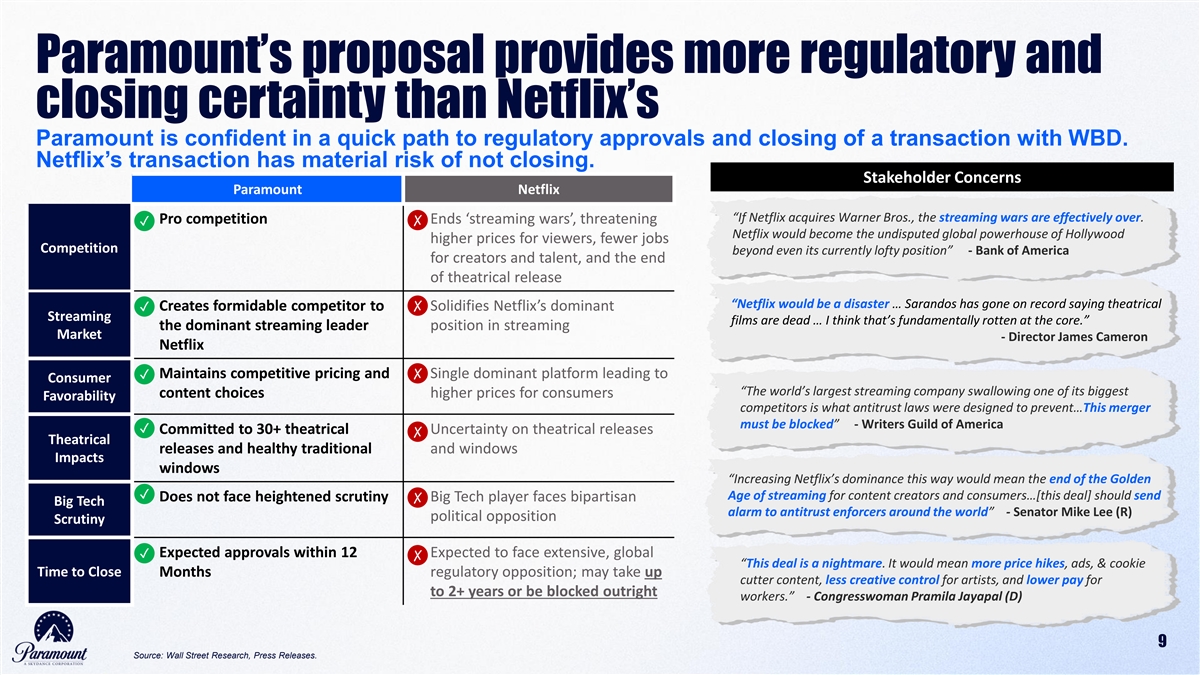

Paramount’s proposal provides more regulatory and closing certainty than Netflix’s Paramount is confident in a quick path to regulatory approvals and closing of a transaction with WBD. Netflix’s transaction has material risk of not closing. Stakeholder Concerns Paramount Netflix “If Netflix acquires Warner Bros., the streaming wars are effectively over. • Pro competition • Ends ‘streaming wars’, threatening ✓✗ Netflix would become the undisputed global powerhouse of Hollywood higher prices for viewers, fewer jobs Competition beyond even its currently lofty position” - Bank of America for creators and talent, and the end of theatrical release “Netflix would be a disaster … Sarandos has gone on record saying theatrical ✗ •✓ Creates formidable competitor to • Solidifies Netflix’s dominant Streaming films are dead … I think that’s fundamentally rotten at the core.” the dominant streaming leader position in streaming Market - Director James Cameron Netflix ✗ •✓ Maintains competitive pricing and • Single dominant platform leading to Consumer “The world’s largest streaming company swallowing one of its biggest content choices higher prices for consumers Favorability competitors is what antitrust laws were designed to prevent…This merger must be blocked” - Writers Guild of America ✓ • Committed to 30+ theatrical • Uncertainty on theatrical releases ✗ Theatrical releases and healthy traditional and windows Impacts windows “Increasing Netflix’s dominance this way would mean the end of the Golden ✓ Age of streaming for content creators and consumers…[this deal] should send • Does not face heightened scrutiny • Big Tech player faces bipartisan ✗ Big Tech alarm to antitrust enforcers around the world” - Senator Mike Lee (R) political opposition Scrutiny •✓ Expected approvals within 12 • Expected to face extensive, global ✗ “This deal is a nightmare. It would mean more price hikes, ads, & cookie Time to Close Months regulatory opposition; may take up cutter content, less creative control for artists, and lower pay for to 2+ years or be blocked outright workers.” - Congresswoman Pramila Jayapal (D) 9 Source: Wall Street Research, Press Releases.

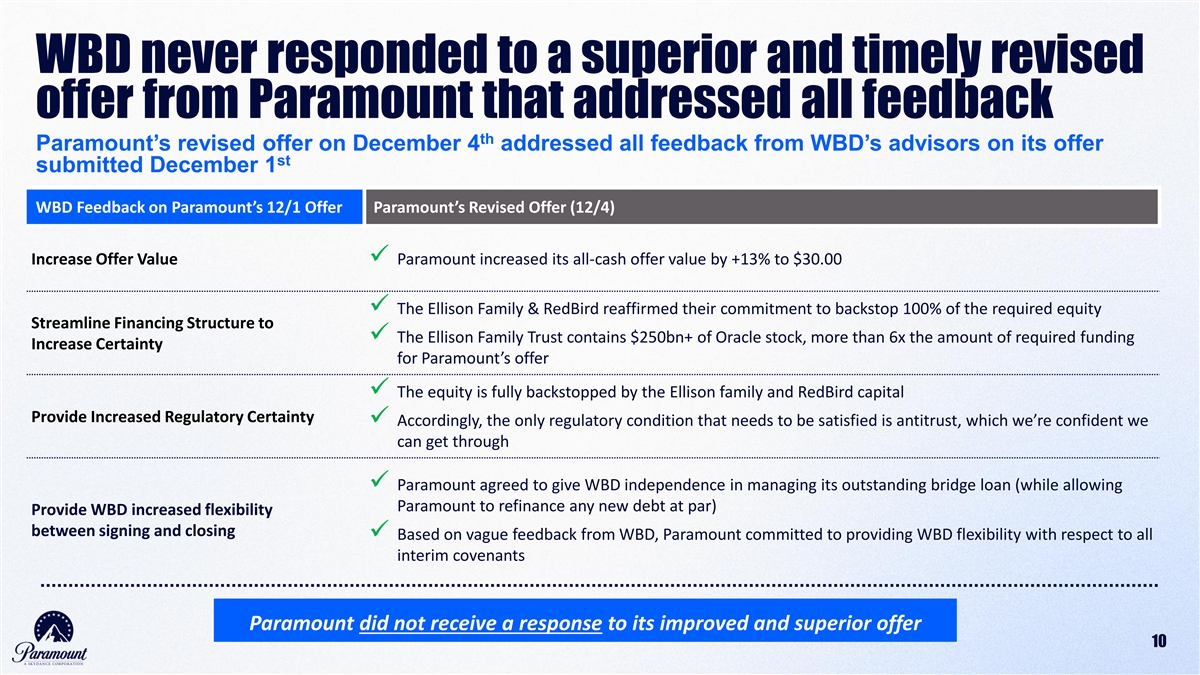

WBD never responded to a superior and timely revised offer from Paramount that addressed all feedback th Paramount’s revised offer on December 4 addressed all feedback from WBD’s advisors on its offer st submitted December 1 WBD Feedback on Paramount’s 12/1 Offer Paramount’s Revised Offer (12/4) Increase Offer Value✓ Paramount increased its all-cash offer value by +13% to $30.00 ✓ The Ellison Family & RedBird reaffirmed their commitment to backstop 100% of the required equity Streamline Financing Structure to ✓ The Ellison Family Trust contains $250bn+ of Oracle stock, more than 6x the amount of required funding Increase Certainty for Paramount’s offer ✓ The equity is fully backstopped by the Ellison family and RedBird capital Provide Increased Regulatory Certainty ✓ Accordingly, the only regulatory condition that needs to be satisfied is antitrust, which we’re confident we can get through ✓ Paramount agreed to give WBD independence in managing its outstanding bridge loan (while allowing Paramount to refinance any new debt at par) Provide WBD increased flexibility between signing and closing ✓ Based on vague feedback from WBD, Paramount committed to providing WBD flexibility with respect to all interim covenants Paramount did not receive a response to its improved and superior offer 10

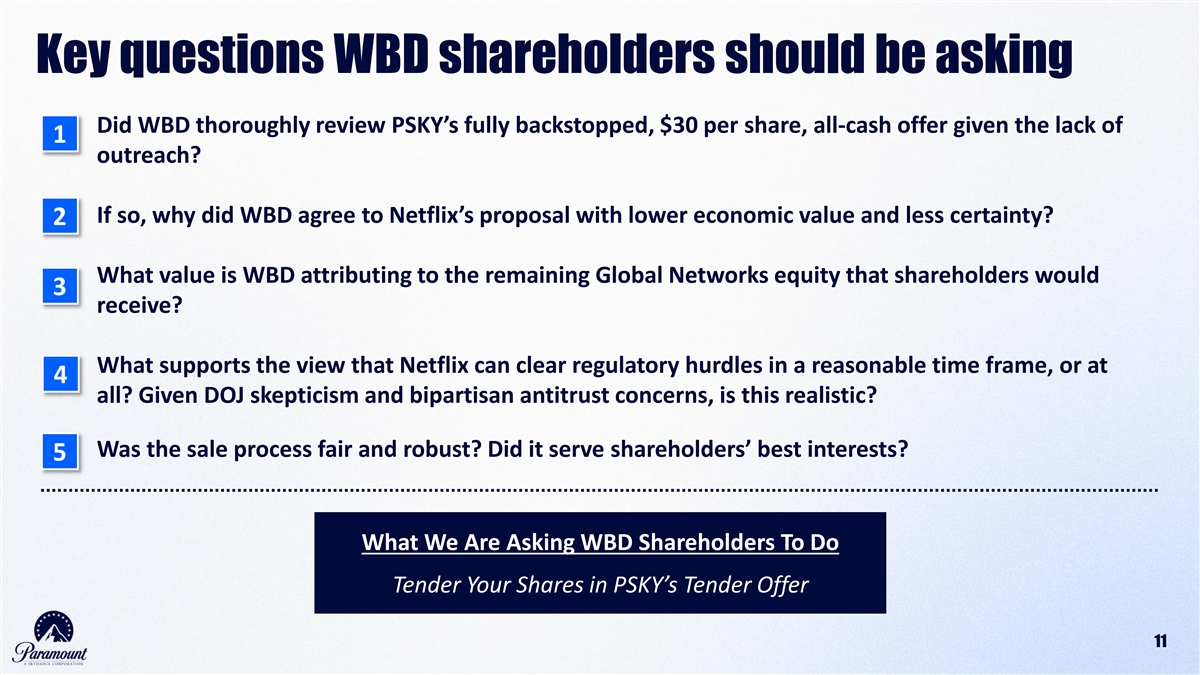

Key questions WBD shareholders should be asking Did WBD thoroughly review PSKY’s fully backstopped, $30 per share, all-cash offer given the lack of 1 outreach? If so, why did WBD agree to Netflix’s proposal with lower economic value and less certainty? 2 What value is WBD attributing to the remaining Global Networks equity that shareholders would 3 receive? What supports the view that Netflix can clear regulatory hurdles in a reasonable time frame, or at 4 all? Given DOJ skepticism and bipartisan antitrust concerns, is this realistic? Was the sale process fair and robust? Did it serve shareholders’ best interests? 5 What We Are Asking WBD Shareholders To Do Tender Your Shares in PSKY’s Tender Offer 11 11

12

Overview of Paramount Proposal

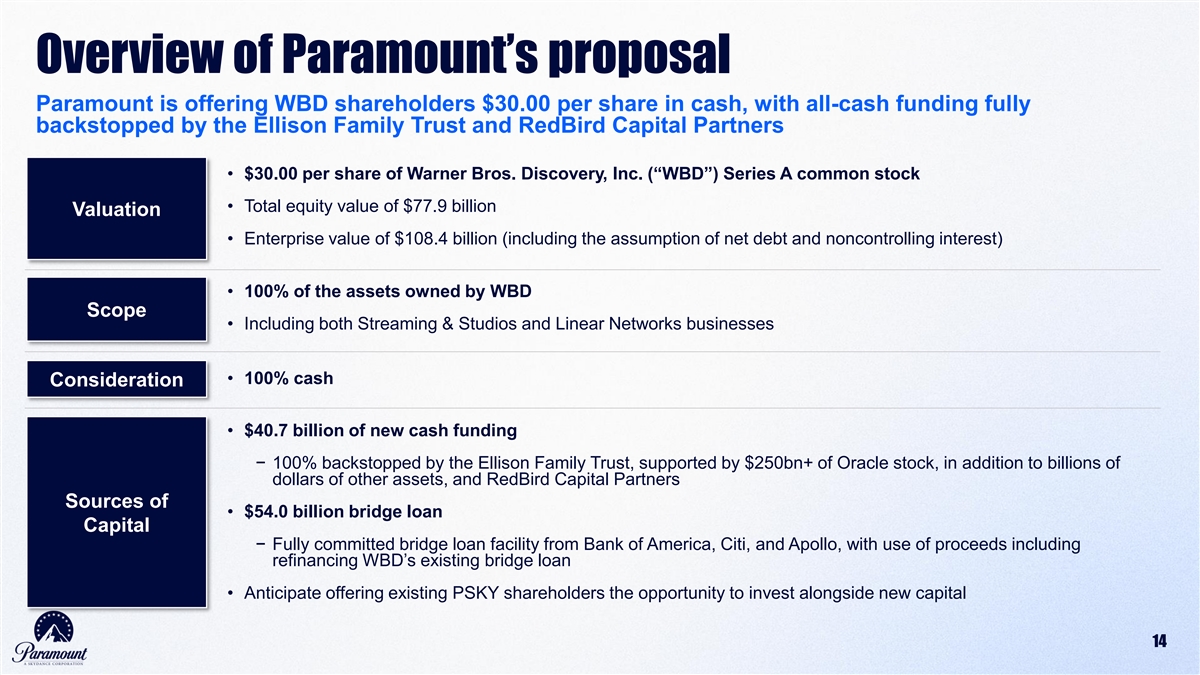

Overview of Paramount’s proposal Paramount is offering WBD shareholders $30.00 per share in cash, with all-cash funding fully backstopped by the Ellison Family Trust and RedBird Capital Partners • $30.00 per share of Warner Bros. Discovery, Inc. (“WBD”) Series A common stock • Total equity value of $77.9 billion Valuation • Enterprise value of $108.4 billion (including the assumption of net debt and noncontrolling interest) • 100% of the assets owned by WBD Scope • Including both Streaming & Studios and Linear Networks businesses • 100% cash Consideration • $40.7 billion of new cash funding − 100% backstopped by the Ellison Family Trust, supported by $250bn+ of Oracle stock, in addition to billions of dollars of other assets, and RedBird Capital Partners Sources of • $54.0 billion bridge loan Capital − Fully committed bridge loan facility from Bank of America, Citi, and Apollo, with use of proceeds including refinancing WBD’s existing bridge loan • Anticipate offering existing PSKY shareholders the opportunity to invest alongside new capital 14

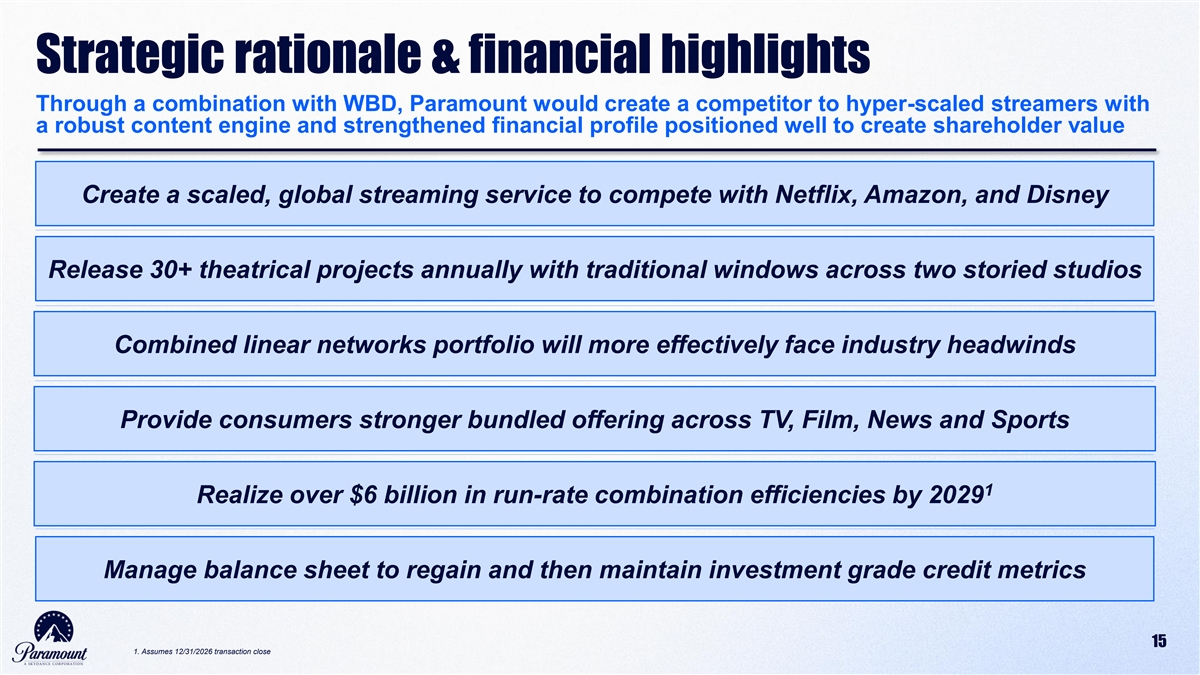

Strategic rationale & financial highlights Through a combination with WBD, Paramount would create a competitor to hyper-scaled streamers with a robust content engine and strengthened financial profile positioned well to create shareholder value Create a scaled, global streaming service to compete with Netflix, Amazon, and Disney Release 30+ theatrical projects annually with traditional windows across two storied studios Combined linear networks portfolio will more effectively face industry headwinds Provide consumers stronger bundled offering across TV, Film, News and Sports 1 Realize over $6 billion in run-rate combination efficiencies by 2029 Manage balance sheet to regain and then maintain investment grade credit metrics 15 1. Assumes 12/31/2026 transaction close

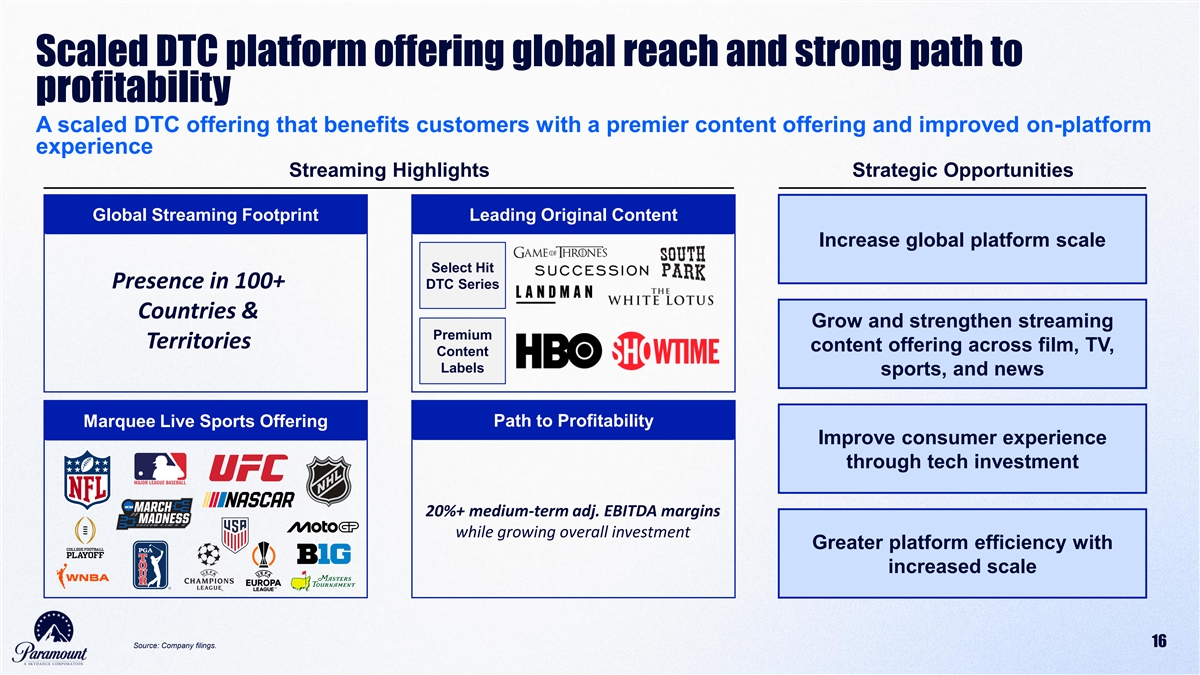

Scaled DTC platform offering global reach and strong path to profitability A scaled DTC offering that benefits customers with a premier content offering and improved on-platform experience Streaming Highlights Strategic Opportunities Global Streaming Footprint Leading Original Content Increase global platform scale Select Hit Presence in 100+ DTC Series Countries & Grow and strengthen streaming Premium Territories content offering across film, TV, Content Labels sports, and news Path to Profitability Marquee Live Sports Offering Improve consumer experience through tech investment 20%+ medium-term adj. EBITDA margins while growing overall investment Greater platform efficiency with increased scale 16 Source: Company filings.

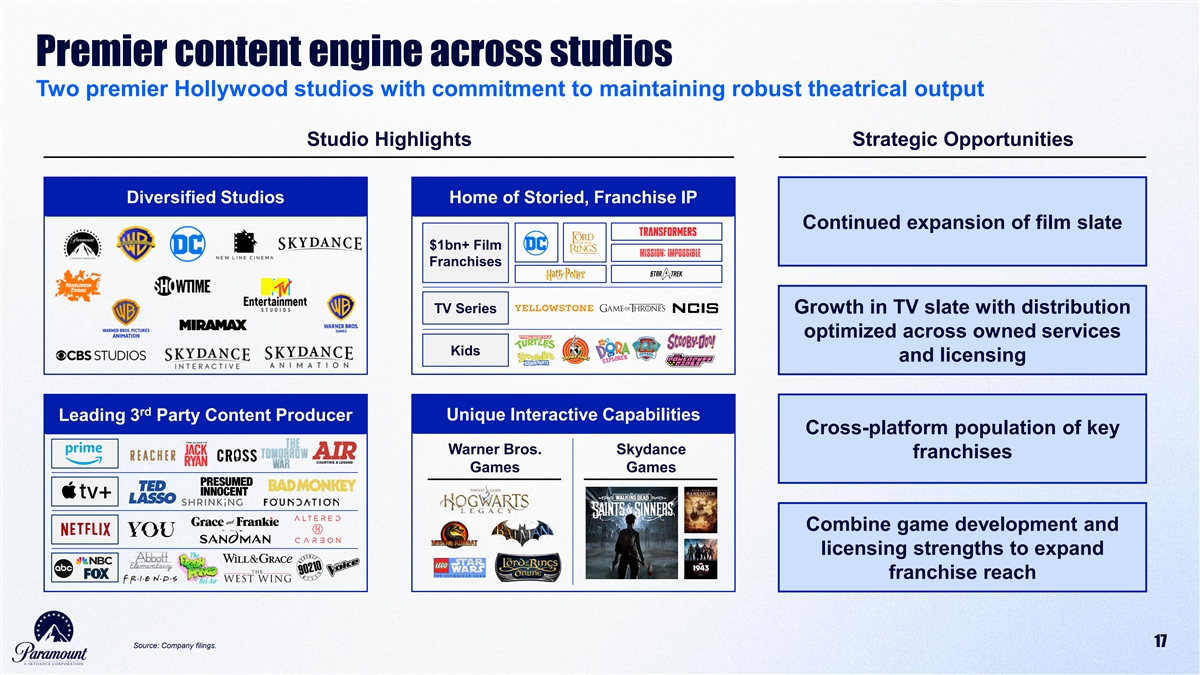

Premier content engine across studios Two premier Hollywood studios with commitment to maintaining robust theatrical output Studio Highlights Strategic Opportunities Diversified Studios Home of Storied, Franchise IP Continued expansion of film slate $1bn+ Film Franchises TV Series Growth in TV slate with distribution optimized across owned services Kids and licensing rd Leading 3 Party Content Producer Unique Interactive Capabilities Cross-platform population of key Warner Bros. Skydance franchises Games Games Combine game development and licensing strengths to expand franchise reach 17 Source: Company filings.

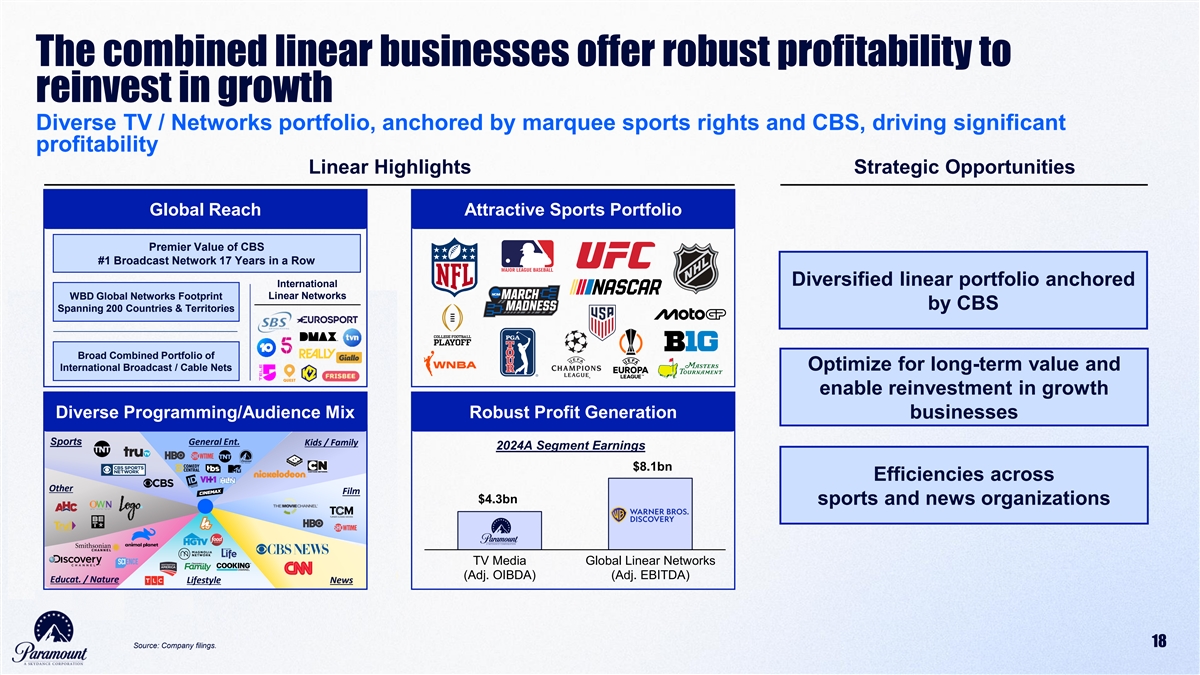

The combined linear businesses offer robust profitability to reinvest in growth Diverse TV / Networks portfolio, anchored by marquee sports rights and CBS, driving significant profitability Linear Highlights Strategic Opportunities Global Reach Attractive Sports Portfolio Premier Value of CBS #1 Broadcast Network 17 Years in a Row Diversified linear portfolio anchored International Linear Networks WBD Global Networks Footprint by CBS Spanning 200 Countries & Territories Broad Combined Portfolio of International Broadcast / Cable Nets Optimize for long-term value and enable reinvestment in growth Diverse Programming/Audience Mix Robust Profit Generation businesses Sports General Ent. Kids / Family 2024A Segment Earnings $8.1bn Efficiencies across Other Film $4.3bn sports and news organizations TV Media Global Linear Networks (Adj. OIBDA) (Adj. EBITDA) Educat. / Nature Lifestyle News 18 Source: Company filings.

THANK YOU

Cautionary Note Regarding Forward-Looking Statements

This communication contains both historical and forward-looking statements, including statements related to Paramount’s future financial results and performance, potential achievements, anticipated reporting segments and industry changes and developments. All statements that are not statements of historical fact are, or may be deemed to be, “forward-looking statements”. Similarly, statements that describe Paramount’s objectives, plans or goals are or may be forward-looking statements. These forward-looking statements reflect Paramount’s current expectations concerning future results and events; generally can be identified by the use of statements that include phrases such as “believe,” “expect,” “anticipate,” “intend,” “plan,” “foresee,” “likely,” “will,” “may,” “could,” “estimate” or other similar words or phrases; and involve known and unknown risks, uncertainties and other factors that are difficult to predict and which may cause Paramount’s actual results, performance or achievements to be different from any future results, performance or achievements expressed or implied by these statements. These risks, uncertainties and other factors include, among others: the outcome of the tender offer by Paramount and Prince Sub Inc. (the “Tender Offer”) to purchase for cash all of the outstanding Series A common stock of WBD or any discussions between Paramount and WBD with respect to a possible transaction (including, without limitation, by means of the Tender Offer, the “Potential Transaction”), including the possibility that the Tender Offer will not be successful, that the parties will not agree to pursue a business combination transaction or that the terms of any such transaction will be materially different from those described herein, the conditions to the completion of the Potential Transaction or the previously announced transaction between Warner Bros. and Netflix Inc. (“Netflix”) pursuant to the Agreement and Plan of Merger, dated December 4, 2025, among Netflix, Nightingale Sub, Inc., Warner Bros. and New Topco 25, Inc. (the “Proposed Netflix Transaction”), including the receipt of any required stockholder and regulatory approvals for either transaction, the proposed financing for the Potential Transaction, the indebtedness Paramount expects to incur in connection with the Potential Transaction and the total indebtedness of the combined companies, the possibility that Paramount may be unable to achieve expected synergies and operating efficiencies within the expected timeframes or at all and to successfully integrate the operations of WBD with those of Paramount, and the possibility that such integration may be more difficult, time-consuming or costly than expected or that operating costs and business disruption (including, without limitation, disruptions in relationships with employees, customers or suppliers) may be greater than expected in connection with the Potential Transaction; risks related to Paramount’s streaming business; the adverse impact on Paramount’s advertising revenues as a result of changes in consumer behavior, advertising market conditions and deficiencies in audience measurement; risks related to operating in highly competitive and dynamic industries, including cost increases; the unpredictable nature of consumer behavior, as well as evolving technologies and distribution models; risks related to Paramount’s decisions to make investments in new businesses, products, services and technologies, and the evolution of Paramount’s business strategy; the potential for loss of carriage or other reduction in or the impact of negotiations for the distribution of Paramount’s content; damage to Paramount’s reputation or brands; losses due to asset impairment charges for goodwill, intangible assets, FCC licenses and content; liabilities related to discontinued operations and former businesses; increasing scrutiny of, and evolving expectations for, sustainability initiatives; evolving business continuity, cybersecurity, privacy and data protection and similar risks; content infringement; domestic and global political, economic and regulatory factors affecting Paramount’s businesses generally, including tariffs and other changes in trade policies; the inability to hire or retain key employees or secure creative talent; disruptions to Paramount’s operations as a result of labor disputes; the risks and costs associated with the integration of, and Paramount’s ability to integrate, the businesses of Paramount Global and Skydance Media, LLC successfully and to achieve anticipated synergies; volatility in the prices of Paramount’s Class B Common Stock; potential conflicts of interest arising from Paramount’s ownership structure with a controlling stockholder; and other factors described in Paramount’s news releases and filings with the Securities and Exchange Commission (the “SEC”), including but not limited to Paramount’s most recent Annual Report on Form 10-K and Paramount’s reports on Form 10-Q and Form 8-K. There may be additional risks, uncertainties and factors that Paramount does not currently view as material or that are not necessarily known. The forward-looking statements included in this communication are made only as of the date of this report, and Paramount does not undertake any obligation to publicly update any forward-looking statements to reflect subsequent events or circumstances.

Additional Information

This communication does not constitute an offer to buy or a solicitation of an offer to sell securities. This communication relates to a proposal that Paramount has made for an acquisition of WBD and the Tender Offer that Paramount, through Prince Sub Inc., its wholly owned subsidiary, has made to WBD stockholders. The Tender Offer is being made pursuant to a tender offer statement on Schedule TO (including the offer to purchase, the letter of transmittal and other related offer documents), filed with the SEC on December 8, 2025. These materials, as may be amended from time to time, contain important information, including the terms and conditions of the offer. Subject to future developments, Paramount (and, if a negotiated transaction is agreed, WBD) may file additional documents with the SEC. This communication is not a substitute for any proxy statement, tender offer statement, or other document Paramount and/or WBD may file with the SEC in connection with the proposed transaction.

Investors and security holders of WBD are urged to read the tender offer statement(s) (including the offer to purchase, the letter of transmittal and other related offer documents), and any other documents filed with the SEC carefully in their entirety if and when they become available as they will contain important information about the proposed transaction. Any definitive proxy statement(s) (if and when available) will be mailed to stockholders of WBD. Investors and security holders will be able to obtain free copies of these documents (if and when available) and other documents filed with the SEC by Paramount through the website maintained by the SEC at http://www.sec.gov.

This communication is neither a solicitation of a proxy nor a substitute for any proxy statement or other filings that may be made with the SEC. Nonetheless, Paramount and its directors and executive officers and other members of management and employees may be deemed to be participants in the solicitation of proxies against the Proposed Netflix Transaction. You can find information about Paramount’s executive officers and directors in Paramount’s Current Reports on Form 8-K filed with the SEC on August 7, 2025, and September 16, 2025, and Paramount’s Quarterly Report on Form 10-Q filed with the SEC on November 10, 2025. Additional information regarding the interests of such potential participants will be included in one or more proxy statements or other documents filed with the SEC if and when they become available. These documents (if and when available) may be obtained free of charge from the SEC’s website at http://www.sec.gov.

Exhibit (a)(5)(C)

CNBC Transcript: Paramount Skydance Chairman & CEO David Ellison Speaks with CNBC’s David Faber on “Squawk on the Street” Today

DAVID FABER: Welcome back to “Squawk on the Street.” I’m David Faber. And I am here now with David Ellison, the chairman and CEO of Paramount, which this morning has launched a $30 all cash tender offer to acquire Warner Bros. Discovery. A company that I believe you bid, at the last count, six times for.

DAVID ELLISON: Correct.

FABER: But did not come up with the prize that you sought, hence this morning’s news. David, why are you doing this?

ELLISON: So, look, we’re really here to finish what we started. Like, just to kind of take you through the road in terms of how we got here. On December 1st, we made an offer to acquire Warner Bros. Discovery to their board, had a conversation with David Zaslav. He came back with a bunch of issues. We then, on December 4th, sent in a bid that addressed every single one of them that is superior to the bid that they signed up. Our offer is $30 a share, all cash, $41 billion in equity that’s backstopped by the Ellison family and RedBird, $54 billion in debt with commitments from Citi, Bank of America and Apollo. We have faster regulatory certainty to close and our deal is pro-consumer. It’s pro-creative talent. It’s pro-competition. And we believe that when you actually to further contextualize the our $30 in cash, or, sorry, $30 a share is basically $17.6 billion in cash, more than the $23 a share that they signed up. We will—

FABER: Right. Well, you’re not obviously paying, you’re paying for global networks. Their deal doesn’t involve paying for global networks, which were traded, it’s a public company. Which, by the way, also figures very prominently here in trying to determine what the overall value of the respective deals are, because they’re a $27.75, including obviously the stock portion of their deal.

ELLISON: Correct.

FABER: But it also includes, well what’s global networks. Is it a $2 stock. Is it a $4 stock. What do you see? Because that can go a long way in terms of at least determining why the board may have said, no, we think Netflix is superior.

ELLISON: So, respectfully, we think that basically that’s valued at $1 a share. I think if you look—

FABER: Why $1?

ELLISON: So, if you look at Versant and where the median of all of this is, it’s about four and a half times. You have to get to five times equity value or more to basically get to the, you know, kind of $3 plus that you’re claiming. But again, I think the most important thing to go back here is, look, we’re sitting on Wall Street where cash is still king. We are offering shareholders $17.6 billion more cash than the deal that they currently have signed up with Netflix. And we believe when they see what is currently in our offer, that that’s what they’ll vote for.

FABER: Were you told during the process that cash is king?

ELLISON: Yes, absolutely. What we were told repeatedly was that they wanted all cash. We delivered all cash. We were, we were asked if they wanted it to be fully backstopped by the Ellison family and RedBird. We delivered it fully backstopped by the Ellison family and RedBird. And when you look at the scale of the companies, right, look at the scale of Netflix, 310 million global subscribers. When you combine the number one streamer with the number three streamer, that creates a company that has

unprecedented market power north of 400 million subscribers. The next largest competitor is Disney, with just under 200 million. That’s bad for Hollywood. That’s bad for the creative community. That’s bad for consumers. And look at how the market is reacting to this deal. We are literally seeing talent talking about the death of movie theaters. We’ve all heard Ted Sarandos’ comments about how he feels about the theatrical experience. And you’ve also seen, you know, and our deal is also offering more cash for shareholders.

FABER: Now, you’ve made that point. And, obviously, it is offering more cash. So, if they said cash is king and then they were willing to take stock, obviously only 14 or 15 percent of the overall consideration that Netflix is offering. Nonetheless, do you feel as though you were disadvantaged in this process? And if you were, what can you cite to prove, in fact, that somehow you were not on a level playing field in having your offer considered with their offer?

ELLISON: So, I do think there is an inherent bias towards us. If you look at it, we, fundamentally—

FABER: Towards them. An inherent bias towards them.

ELLISON: Correct.

FABER: Yes.

ELLISON: We put the company in play.

FABER: Yes.

ELLISON: We, you know, which, again, we don’t think was particularly taken well.

FABER: No, I think that actually starts you off on a potentially bad foot when you’re making an unsolicited bid for a company.

ELLISON: But look at what we did with our last offer. We literally submitted $30 a share in cash. Never got a phone call. Never got a single markup of basically our merger agreement. Never got a response. And that’s why we’re here today. We’re here to finish, to make sure that we can take directly to shareholders the offer that we sent to the board.

FABER: So you never got a response from that last—

ELLISON: Not one time.

FABER: And did you indicate that that was best and final at the time, or perhaps say that it wasn’t?

ELLISON: No. So, actually, the last communication that I had with David Zaslav is I made it incredibly clear in text message, this is all going to be public for everybody to see, that we addressed all of the issues that they asked for, and very specifically that our offer was not best and final. And so, when we literally delivered a $30 per share all cash offer, we never heard back.

FABER: You never, you never heard back from them at all. You know, a lot of this goes back, of course, and you mentioned it already, to the perceived risks of antitrust rejection. Certainly on the Netflix side. It’s still an issue as well for every deal, including your own perhaps, state A.G.s and the like. It comes back to Donald Trump oftentimes because of sort of his unique place in this administration. And he even indicated yesterday at the Kennedy Center he would be involved in this decision. Have you gotten any assurances from him in the sense of your own deal would pass antitrust muster and/or that Netflix’s transaction would not?

ELLISON: So, David, I think you have to look at this basically on the merits, right? We are trying to combine the number four streamer with the number five streamer. When you put Paramount and HBO Max together, you get round numbers, 200 million subscribers. That creates a streaming service that is competitive with Disney. When you put number one and number three together, you are handing Netflix unprecedented market power, which is anti-competitive in every single measure, every single metric you can measure. And we think that is bad. Again, it’s bad for the consumer. It’s bad for the creative community. This deal, if it is allowed to move forward, will actually be the death of the theatrical movie business in Hollywood. We’re sitting here today trying to save it.

FABER: Understood. It’s going to be a little while. This is going to be a fight that stretches, perhaps until the shareholder vote, until shareholders are heard from, unless their voices are heard prior and Warner Bros. makes a different decision. I am curious, though. You know, you’re going to war here, so to speak, with Netflix, an incredibly well-endowed company that has the ability, it would seem, to choose to raise its offer even more. Why bother when they conceivably could simply come back and raise their offer if they need to?

ELLISON: So, again, I think when you actually look at what the highest offer that is currently on the table, $30 in cash, the last time I checked, beats $23 in cash. And that’s $17.6 billion in cash more so, as we’ve said. We believe we have the superior offer. We’re taking that directly to shareholders. And we think that’s what they’re going to vote for.

FABER: I know, but that’s not a fair comparison. I mean there is stock. Netflix stock is worth right, it’s in, within the collar, it’s worth at least 3.50 a share to the deal. I mean saying our cash versus theirs doesn’t seem a fair comparison, David.

ELLISON: So, respectfully, I disagree. I mean, look, I mean, look, those shareholders can basically go buy Netflix cash on the, sorry, Netflix stock in the open market if they want to, and they’re going to be sitting there with a linear stub that’s valued at $1 a share, which is a business that’s in secular decline that without the synergies that’s basically created by our deal, they will ultimately be holding something that is not worth anything. By every metric you can look at, we believe that our offer is superior to shareholders.

FABER: Right, and again, we’re going to get a lot of debate around the value of that stub, because even though it’s an incremental, let’s call it difference of a $2 it can go to the to the value judgment. Let me ask you about Paramount though, if in fact, you are successful here. You’re taking on a lot of debt, right? I mean, it’s and you’re diluting your own shareholders significantly through an inclusion of what $41 billion in equity. Isn’t that correct?

ELLISON: Yeah. But look one, we’re the largest shareholder of the, of basically the Paramount Class B common stock.

FABER: We being?

ELLISON: We being the Ellison family, we will also be the largest investor in this deal. We’re literally sitting here today because we are fighting for our shareholders, and we’re also fighting for the shareholders of Warner Bros. Discovery. And from that standpoint, this deal is accretive to our shareholders. You know, when you look at what the combined business would be with the synergies that you put through it, round numbers, $70 billion in top line revenue, we get to $16 billion in EBITDA very quickly, and it generates $10 billion in cash flow. What we’re creating by putting these two companies together is a real competitor to Netflix, a real competitor to Amazon, a real competitor to Disney, not something that is so anti-competitive. There will be no more competition in Hollywood if this deal is allowed to come to pass.

FABER: Is it an existential issue for you though, if you don’t succeed here, David?

ELLISON: Look, as we’ve said in our on our earnings call, we believe in our standalone business. We have a great plan. But very simply, we made the highest offer for the company, $30 in cash is more than $23.

FABER: Right, but when it comes to Paramount itself, if you aren’t successful here, you have confidence that you still have the scale? I mean, we’ve had this conversation before.

ELLISON: Yeah, yeah.

FABER: I would assume that you’re going to try and figure something else out because there is a sense that you don’t have the scale to compete in this world.

ELLISON: As we’ve said, we can absolutely this is a buy versus build. We absolutely have a path to be able to build. But again, we actually sit here today having put forth the most value for shareholders for Warner Bros. Discovery, we believe that they need to be able to evaluate that offer, and that’s why we’re taking it directly to the shareholders.

FABER: I asked you about the President, but I’d love to come back to that. I mean, do you sense that he is in your corner here?

ELLISON: What I would say is I’m incredibly grateful for the relationship that I have with the President, and I also believe he believes in competition. And when you fundamentally look at the marketplace, allowing the number one streaming service to combine with the number three streaming service is anti-competitive, and this whole notion of category ambiguity, forgive me, David, you’ve been doing this a long time.

FABER: Yes, I have.

ELLISON: Like I don’t, I don’t buy it.

FABER: You don’t buy it. In other words, their argument, John Malone made this argument with me. It’s not about streamers, it’s about TikTok and Instagram and YouTube.

ELLISON: I’m sorry this is that’s that’s, let’s follow that analogy for a second, right? Okay, that’s like saying Coke can buy Pepsi, that they’re both beverages because Budweiser is a substitute for Coke. That’s not a realistic argument. Now let’s actually look at it from the talent community, the greatest showrunners in the world. David Benioff is not going to take the next Game of Thrones to basically TikTok or to Instagram. They’re going to take it to Netflix. They’re going to take it to Amazon. They’re going to take it to Apple, they’re going to take it to HBO Max. They’re going to take it to Paramount Plus. That’s not actually how the ecosystem works. If this deal is allowed to come to pass, it is anti-competitive, and it is a horrible deal for Hollywood. And as someone who spent the last 15 years of my life producing movies and television shows, this is an industry that I love, this is an existential moment for our business, and we believe that what we are offering is better for Hollywood. It’s better for the customers and it’s pro-competitive.

FABER: You know, I wonder we were having this conversation on the desk a moment ago. It may be better for Hollywood than Netflix owning it, but will it be better in and of itself? I mean, you’re talking about huge cost synergies, for example. It’s not clear or can you make it clear that, in fact, Hollywood will actually benefit, and there won’t be reductions overall still in the amount of productions and jobs.

ELLISON: Absolutely it will be beneficial for Hollywood. I mean, one, everyone loves to contextualize the six legacy studios, right? But I think when you have to look at the new entries that have come into the place, Apple is now in the business, Netflix is now in the business, Amazon is now in the business. What we are, what we are buying by our basically acquisition of Warner Bros. Discovery is we are accelerating our path to scale. What Netflix is buying is unprecedented market power that will kill competition in the industry. What we are doing will create another scaled, healthy buyer for the creative community and for talent. We’ll put 30 movies a year in theaters, exclusively.

FABER: 30 movies, I mean, because right now at Paramount, you’re nowhere near—

ELLISON: But look at what we’re doing at Paramount. When we bought the company, eight movies a year. We’re going to release 15 movies a year, next year, and we’re going to grow that. We’ve said it publicly, that we want to grow it to 20. We believe that the number one way in the movie business to create valuable intellectual property is to release movies in theaters, not at home. We deeply believe in that experience. And when you think about the generational heirlooms that have been passed down from generation to generation that are that’s filmed entertainment, those are movies that you saw in the theater.

FABER: You know, the news business comes up for a moment here. I mean, you’re going to own linear cable assets, obviously, CNN amongst them, if you are successful here. Thank you for the mention of Versant, by the way, and in a favorable light, but the business is in steep decline. There’s no way around that. Why do you want to own these assets given what are significant reductions? I think the plan that even came from Warner Bros. in the discussion with you talks about what 60% percent top line reduction over at least two years.

ELLISON: Absolutely so the reason why we believe basically in this combination is very simply, by putting the creative content engines of the companies together, we believe we can win in content. We’d have an IP portfolio that’s competitive with Disney by putting Paramount and Warner Bros. together. It accelerates our north star goal of getting to scale and streaming, and we get to basically round numbers, 200 million subscribers as a result of this, which, again, from a competitive standpoint, is over 100 million below Netflix and Amazon. And then when you look at the linear portfolio, there are significant synergies. And when you look at what we can do with CBS, which is a crown jewel asset, and again, all linear is not equivalent, right? I mean, broadcast is an incredibly stable, healthy business. Cable is in secular decline, by the way, being replaced by streaming. Back to your why I don’t buy the category ambiguity conversation.

FABER: Right.

ELLISON: But basically, when we can combine it with our portfolio, we believe we can bend the linear curve, have that linear business be incredibly cash flow generative, which we can then take and invest into more content to grow the growth areas of our business, which is the movies we’re going to make, the streaming series we’re going to make, the sports we’re going to invest in. And again, this creates a scaled competitor, not something that is so anti-competitive. It’ll be the end of the industry, as we know it.

FABER: Why not just let the process run out and sit around and wait if you’re really so confident that Netflix can’t get antitrust?

ELLISON: So I think if you look at basically how long it’ll take them to go through antitrust and the $5.8 billion break fee—

FABER: Reverse break fee.

ELLISON: Yeah, yeah, but basically, if you think about that, if this takes two years, and I think, and you’ve seen reports on this, that this has basically been a defensive move by Netflix, and if they actually slow down our scale for the next two years, that’s a win for them. That, by nature, is anti-competitive.

FABER: Right, a couple of real quick things before we wrap up. I mean, CNN, I assume you would combine the news gathering operation with CBS’s, if, in fact, you did own that asset.

ELLISON: Yeah. So look, we’ve been really clear since by the last time we’re here, what we want to do with news, which is, we want to build a scaled news service that is basically, fundamentally in the trust business, that is in the truth business, and that speaks to the 70% of Americans that are in the middle. And we believe that by doing so that is for us, kind of doing well while doing good. And we believe in that business model, and we believe it’s essential.

FABER: And do you, do you think the President embraces the idea of you being the owner of CNN, given his criticism, obviously, for that network in the past?

ELLISON: By the way, we’ve had great conversations with the President about this, but I think, what, but I don’t want to speak for him in any way, shape or form.

FABER: Mid east investors have figured into some of the reporting here. Are they a part of that $41 billion in equity?

ELLISON: Look, we absolutely have strategic partners in this deal, but I want to be really clear, the last deal that we submitted was fully backstop the equity by the Ellison family and RedBird. There has never been a financing condition in any deal that we submitted to the board of Warner Bros. Discovery, and we are standing behind them.

FABER: So when I hear from the other side that they were uncertain as to who potentially to come after in terms of the entities that were submitting the bid, if, in fact, you didn’t close, that was an argument that I’ve heard. What’s your response?

ELLISON: It just happens to be categorically false. Again, this is all now public. The last offer that we submitted to the board the equity $41 billion was fully backstopped by the Ellison family and RedBird Capital Partners. We had debt commitments from Bank of America, Citi and Apollo for the full $54 billion so the notion of that claim is just categorically false. It’s fiction.

FABER: And does it go back to then your contention that somehow you didn’t get a fair shake?

ELLISON: Well, I think when you actually look at this on the merits, it’s what we, it’s what it’s what I started with, $30 a share in cash is more than $23. This is a better deal for shareholders, and it also has a clear path to close. Very simply, our deal basically, is more value, it’s more certainty, and it’s more speed to close, and we think that’s what shareholders are going to vote on.

FABER: We got an opening bell that you and I can hear as well. I want to continue briefly for a bit more if we can. David, you know what happens from here? What are your expectations now that you’re obviously going to be speaking directly to shareholders as to what may happen?

ELLISON: Well, I mean, I think when shareholders actually see the offer that we put on the table. I mean, look, we still haven’t gotten a response from the Warner board for the $30 in cash that we offered, and that’s the highest offer that’s currently on the table. And we again, as we said, we believe that’s what shareholders are going to pay.

FABER: You know, again, coming back to this highest offer on the table. I mean, they would argue that $27.75, which it’s currently worth right now, because the stock is staying in the collar, plus, what their argument would be is, let’s call it three bucks for global networks, equals a higher number than your number.

ELLISON: It’s, again, I think, if you actually look at that, and if you, if you look at the math and the amount of debt, I mean, basically on what we could extrapolate from the information we looked at, that linear business is going to have $15 billion of debt on it. It’s an entirely a cable portfolio that is in secular decline, and every single day it’s worth less money than it is right now. Our deal basically provides a significant amount of synergies and sports rights that will be able to obviously perfect protect those linear properties, having that sit out there on their own, again, I think it’s gonna be worth a lot less than people are claiming.

FABER: David, what do you think if you’re correct, and again, this is yet to be determined, but if you’re correct that you were somehow disadvantaged in this process after starting it in an unsolicited fashion and making bid after bid after bid, why, why do you think if you’re correct in that assumption that that was the case?

ELLISON: Again, let’s just, let’s just go back to the facts right? The day before the deal was announced, we submitted a bid to the Warner Bros., to Warner Bros., that was $30 a share, all cash that delivered the 100% cash that they asked for, that delivered higher value, that delivered basically regulatory, you know, obviously faster path to regulatory certainty, and we never heard back. We’re here to finish the process.

FABER: Right, no, I know that. The reason I’m asking you never heard back. Do you think, why? Why, why in your you have to have thought about this. Why are we somehow being disadvantaged? What’s the answer?

ELLISON: Look, we’ve been asking ourselves that same question, which is why we’re taking this directly to shareholders.

FABER: So you don’t know the answer.

ELLISON: Look, we do believe that there has been an inherent bias in this process, because, again, to make a $30 all cash offer and to literally text the CEO that our offer is not best and final, and then to not hear back. What do you think the answer is?

FABER: But you know, I’ve been trying to understand it as well and trying to fully understand how many board members because they have a lot of very talented board members at this company were completely informed of everything that had occurred. And I’ve heard the idea that somehow you were told that your deal wasn’t perfected. Is that correct?

ELLISON: So by the way, we’ve heard that but, but again, it just, it has no basis in reality. It’s why I keep going back to the $41 billion in equity was fully backstopped by the Ellison family and RedBird.

FABER: Is your father selling Oracle stock, by the way, to finance that, or just margining it? How is that actually working?

ELLISON: So, so we obviously have investors that we’re partnering with as well. But again, we’re fully, we have all the capital necessary to complete this transaction.

FABER: Well, when you say that, though, is there, is there a way that they could perhaps doubt that, because it doesn’t involve selling stock and actually having the money on hand?

ELLISON: David, come on, please. Like, I think, I think kind of calling that into question is, is I don’t think there’s any merit to that.

FABER: No, I think, I think that’s a fair point on your part, but they might ask it. I mean, you know, maybe they already have.

ELLISON: Again, the equity was fully backstopped.

FABER: David, you know, it’s going to be an interesting fight, obviously, as it stretches out conceivably, over these next few months. And we certainly appreciate your taking time. I guess you’re going to continue to communicate, and or your team will continue to communicate the merits of your deal. Do you ever see raising your offer overall?

ELLISON: Again right now, I think our offer is currently the highest on the table, and we’re still waiting to hear back from that offer. David, appreciate you taking the time.

FABER: Thank you.

ELLISON: Thank you.

Cautionary Note Regarding Forward-Looking Statements

This communication contains both historical and forward-looking statements, including statements related to Paramount’s future financial results and performance, potential achievements, anticipated reporting segments and industry changes and developments. All statements that are not statements of historical fact are, or may be deemed to be, “forward-looking statements”. Similarly, statements that describe Paramount’s objectives, plans or goals are or may be forward-looking statements. These forward-looking statements reflect Paramount’s current expectations concerning future results and events; generally can be identified by the use of statements that include phrases such as “believe,” “expect,” “anticipate,” “intend,” “plan,” “foresee,” “likely,” “will,” “may,” “could,” “estimate” or other similar words or phrases; and involve known and unknown risks, uncertainties and other factors that are difficult to predict and which may cause Paramount’s actual results, performance or achievements to be different from any future results, performance or achievements expressed or implied by these statements. These risks, uncertainties and other factors include, among others: the outcome of the tender offer by Paramount and Prince Sub Inc. (the “Tender Offer”) to purchase for cash all of the outstanding Series A common stock of WBD or any discussions between Paramount and WBD with respect to a possible transaction (including, without limitation, by means of the Tender Offer, the “Potential Transaction”), including the possibility that the Tender Offer will not be successful, that the parties will not agree to pursue a business combination transaction or that the terms of any such transaction will be materially different from those described herein, the conditions to the completion of the Potential Transaction or the previously announced transaction between Warner Bros. and Netflix Inc. (“Netflix”) pursuant to the Agreement and Plan of Merger, dated December 4, 2025, among Netflix, Nightingale Sub, Inc., Warner Bros. and New Topco 25, Inc. (the “Proposed Netflix Transaction”), including the receipt of any required stockholder and regulatory approvals for either transaction, the proposed financing for the Potential Transaction, the indebtedness Paramount expects to incur in connection with the Potential Transaction and the total indebtedness of the combined companies, the possibility that Paramount may be unable to achieve expected synergies and operating efficiencies within the expected timeframes or at all and to successfully integrate the operations of WBD with those of Paramount, and the possibility that such integration may be more difficult, time-consuming or costly than expected or that operating costs and business disruption (including, without limitation, disruptions in relationships with employees, customers or suppliers) may be greater than expected in connection with the Potential Transaction; risks related to Paramount’s streaming business; the adverse impact on Paramount’s advertising revenues as a result of changes in consumer behavior, advertising market conditions and deficiencies in audience measurement; risks related to operating in highly competitive and dynamic industries, including cost increases; the unpredictable nature of consumer behavior, as well as evolving technologies and distribution models; risks related to Paramount’s decisions to make investments in new businesses, products, services and technologies, and the evolution of Paramount’s business strategy; the potential for loss of carriage or other reduction in or the impact of negotiations for the distribution of Paramount’s content; damage to Paramount’s reputation or brands; losses due to asset impairment charges for goodwill, intangible assets, FCC licenses and content; liabilities related to discontinued operations and former businesses; increasing scrutiny of, and evolving expectations for, sustainability initiatives; evolving business continuity, cybersecurity, privacy and data protection and similar risks; content infringement; domestic and global political, economic and regulatory factors affecting Paramount’s businesses generally, including tariffs and other changes in trade policies; the inability to hire or retain key employees or secure creative talent; disruptions to Paramount’s operations as a result of labor disputes; the risks and costs associated with the integration of, and Paramount’s ability to integrate, the businesses of Paramount Global and Skydance Media, LLC successfully and to achieve anticipated synergies; volatility in the prices of Paramount’s Class B Common Stock; potential conflicts of interest arising from Paramount’s ownership structure with a controlling stockholder; and other factors described in Paramount’s news releases and filings with the Securities and Exchange Commission (the “SEC”), including but not limited to Paramount’s most recent Annual Report on Form 10-K and Paramount’s reports on Form 10-Q and Form 8-K. There may be additional risks, uncertainties and factors that Paramount does not currently view as material or that are not necessarily known. The forward-looking statements included in this communication are made only as of the date of this report, and Paramount does not undertake any obligation to publicly update any forward-looking statements to reflect subsequent events or circumstances.

Additional Information

This communication does not constitute an offer to buy or a solicitation of an offer to sell securities. This communication relates to a proposal that Paramount has made for an acquisition of WBD and the Tender Offer that Paramount, through Prince Sub Inc., its wholly owned subsidiary, has made to WBD stockholders. The Tender Offer is being made pursuant to a tender offer statement on Schedule TO (including the offer to purchase, the letter of transmittal and other related offer documents), filed with the SEC on December 8, 2025. These materials, as may be amended from time to time, contain important information, including the terms and conditions of the offer. Subject to future developments, Paramount (and, if a negotiated transaction is agreed, WBD) may file additional documents with the SEC. This communication is not a substitute for any proxy statement, tender offer statement, or other document Paramount and/or WBD may file with the SEC in connection with the proposed transaction.

Investors and security holders of WBD are urged to read the tender offer statement(s) (including the offer to purchase, the letter of transmittal and other related offer documents), and any other documents filed with the SEC carefully in their entirety if and when they become available as they will contain important information about the proposed transaction. Any definitive proxy statement(s) (if and when available) will be mailed to stockholders of WBD. Investors and security holders will be able to obtain free copies of these documents (if and when available) and other documents filed with the SEC by Paramount through the website maintained by the SEC at http://www.sec.gov.

This communication is neither a solicitation of a proxy nor a substitute for any proxy statement or other filings that may be made with the SEC. Nonetheless, Paramount and its directors and executive officers and other members of management and employees may be deemed to be participants in the solicitation of proxies against the Proposed Netflix Transaction. You can find information about Paramount’s executive officers and directors in Paramount’s Current Reports on Form 8-K filed with the SEC on August 7, 2025, and September 16, 2025, and Paramount’s Quarterly Report on Form 10-Q filed with the SEC on November 10, 2025. Additional information regarding the interests of such potential participants will be included in one or more proxy statements or other documents filed with the SEC if and when they become available. These documents (if and when available) may be obtained free of charge from the SEC’s website at http://www.sec.gov.

Exhibit (a)(5)(D)

Paramount Skydance Corporation

NasdaqGS:PSKY

M&A Call

Monday, December 8, 2025 3:30 PM GMT

| COPYRIGHT © 2025 S&P Global Market Intelligence, a division of S&P Global Inc. All rights reserved. spglobal.com/marketintelligence |

1 |

Contents

Table of Contents

| Call Participants |

3 | |||

| Presentation |

4 | |||

| Question and Answer |

8 |

| COPYRIGHT © 2025 S&P Global Market Intelligence, a division of S&P Global Inc. All rights reserved. spglobal.com/marketintelligence |

2 |

PARAMOUNT SKYDANCE CORPORATION M&A CALL DEC 08, 2025

Call Participants

EXECUTIVES

Andrew M. Gordon

Chief Strategy Officer, COO & Director

David Ellison

Chairman & CEO

Kevin Creighton

EVP of Corporate Finance & Investor

Relations

ANALYSTS

Benjamin Daniel Swinburne

Morgan Stanley, Research Division

Jessica Jean Reif Ehrlich Cohen

BofA Securities, Research Division

Richard Scott Greenfield

LightShed Partners, LLC

Robert S. Fishman

MoffettNathanson LLC

Steven Lee Cahall

Wells Fargo Securities, LLC, Research

Division

Unknown Analyst

| Copyright © 2025 S&P Global Market Intelligence, a division of S&P Global Inc. All Rights reserved. spglobal.com/marketintelligence |

3 |

PARAMOUNT SKYDANCE CORPORATION M&A CALL DEC 08, 2025

Presentation

Operator

Good morning. My name is Nadia, and I’ll be the conference operator today. At this time, I would like to welcome everyone to Paramount management call to discuss the launch of their all-cash tender offer to acquire Warner Bros. Discovery. [Operator Instructions] I would now like to turn the call over to Kevin Creighton, Paramount’s EVP of Investor Relations. You may now begin your conference call.

Kevin Creighton

EVP of Corporate Finance & Investor Relations

Good morning, and thank you for taking the time to join us today. I’m Kevin Creighton, EVP of Corporate Finance and Investor Relations. Joining me today is our Chairman and Chief Executive Officer; David Ellison; and our Chief Strategy and Operating Officer, Andy Gordon.

As a reminder, we will be making forward-looking statements today. The forward-looking statements include statements concerning the proposed transaction between Paramount and Warner Bros. Discovery, including with respect to the expected timing, the completion and the effects thereof.

All forward-looking statements involve known and unknown risks, uncertainties and other factors that are difficult to predict and which may cause Paramount’s actual results, performance or achievements to be different from any future results, performance or achievements expressed or implied by these statements. Additional information is available in our SEC filings. Additionally, we will be posting materials to our IR website at the conclusion of this call.

With that, I’ll turn it over to David.

David Ellison

Chairman & CEO

Hello, everyone. Thank you all for joining us today, especially on such short notice. This morning, we advanced our proposal to acquire Warner Bros. Discovery by filing a tender offer, and we will submit our HSR filing here in the U.S., and we are also getting ready for the regulatory processes started internationally.

Consistent with the formal proposal we delivered to the Warner Bros. Discovery Board on December 4, we are offering $30 per share, all cash fully backstopped by my family, RedBird Capital Partners and our partners at Bank of America, Citi Bank and Apollo.

As part of our offer, the Ellison family and RedBird would remain the majority shareholders with an owner-operator ethos and discipline. Our offer represents approximately $18 billion in additional cash, certainty beyond Netflix’s offer, which is a cash consideration of $23.25 per share, as we offer far greater certainty, both in terms of the regulatory path and the economics of an all- cash transaction.

On Thursday, we submitted our fully financed superior offer, an offer that directly addressed every concern with our previous bid that they laid out, yet we did not receive a single call back. That brings us here today. We want to bring our proposal directly to WBD shareholders to evaluate a clearly superior proposal across both economic value and regulatory certainty. And we believe they deserve that choice. We’re here to fight for value for our shareholders and for WBD shareholders.

The motivation for this effort is simple. It’s the same reason we pursued Warner Bros. Discovery from the start. We love the movie and entertainment business. We believe deeply in its future, and we want to help preserve and strengthen it.

Movies are one of America’s greatest exports, and we want to lean into that legacy, not diminish it. By bringing together the complementary strengths of Paramount and Warner Bros. Discovery, we can unlock greater scale, reach and create a potential, telling even better stories and sharing them with a broader global audience.

This transaction is about building more, not cutting back, more opportunity for the industry, more choice for consumers, more value for shareholders and more support for creative talent. Our focus is on expanding creative output, not dominating the sector as Netflix envisions. Our goal is to make Hollywood stronger in a way that benefits the entire ecosystem.

| Copyright © 2025 S&P Global Market Intelligence, a division of S&P Global Inc. All Rights reserved. spglobal.com/marketintelligence |

4 |

PARAMOUNT SKYDANCE CORPORATION M&A CALL DEC 08, 2025

We’re taking our offer directly to shareholders because they deserve transparency and the ability to make an informed decision. Our proposal is superior to Netflix’s in every dimension, higher headline value, increased certainty in that value, greater regulatory certainty and a pro-Hollywood, pro-consumer and pro competition future. We’re confident that once shareholders have the opportunity to choose for themselves, they’ll choose Paramount.

Now we’ll take a few minutes to talk through some slides that highlight some key points. These will be made available on the IR website at the conclusion of this call.